If you're reselling on Vinted in the Netherlands, understanding VAT rules is essential. Here's a quick breakdown:

- Occasional Sellers: Selling personal items occasionally? VAT usually doesn't apply.

- Professional Resellers: Selling regularly or for profit? VAT registration and compliance are mandatory. Vinted requires these sellers to register as "Pro Sellers", though sellers pay no fees under the platform's European model.

- DAC7 Reporting: Platforms like Vinted must report seller data to tax authorities if you exceed 30 transactions or €2,000 in sales annually.

Key VAT rules include:

- Thresholds: Dutch VAT registration starts at €20,000 turnover in 12 months.

- Cross-Border Sales: Exceeding €10,000 in EU sales means applying the buyer's VAT rate. Use the One-Stop Shop (OSS) to simplify reporting.

- Margin Scheme: For reselling used goods, VAT is calculated on profit only, not the full sale price.

Non-compliance risks include account suspension, fines, and backdated taxes. Accurate record-keeping is critical for VAT filings and audits. For more ways to optimize your shop, check out these essential Vinted tips for professional success.

VAT in Europe: Guide to EU VAT and IOSS for online sellers

sbb-itb-d4aa959

DAC7 Reporting Requirements for Vinted Resellers

When it comes to VAT compliance, understanding DAC7 reporting requirements is a key step for resellers on platforms like Vinted. This ensures transparency and helps avoid unnecessary penalties.

What is DAC7?

DAC7 (Council Directive (EU) 2021/514) is a regulation introduced by the EU, effective from 1 January 2023. Its primary goal is to improve tax transparency by requiring digital platforms like Vinted to collect and report seller information to tax authorities. This ensures income earned through online platforms aligns with existing national tax rules. Platforms must submit this data annually by 31 January for the previous calendar year. The information is then automatically shared between EU Member States.

It’s important to note that DAC7 doesn’t create new taxes. According to the European Commission:

"DAC7 does not impose any new tax or in any way regulate the taxation of income earned by sellers on digital platforms. Income earned by sellers on digital platforms is taxed in accordance with the existing taxation rules of the EU country based on their national legislation."

Thresholds Triggering DAC7 Reporting

Vinted is required to report your sales data if you exceed specific thresholds in a calendar year. The information shared includes your name, address, Tax Identification Number (TIN), VAT ID (if applicable), bank details, quarterly sales, transaction counts, and any fees withheld. The first automatic exchange of this data between EU Member States occurred in February 2024.

| Seller Type | Transaction Count | Revenue Amount |

|---|---|---|

| Private Sellers | More than 30 transactions per year | Total consideration exceeding €2.000,00 per year |

| Business Sellers | Always reported (no minimum threshold) | Always reported (no minimum threshold) |

How DAC7 Affects Resellers

For Vinted resellers, DAC7 brings a new level of visibility to your sales activities. Tax authorities now rely on automated systems to match platform reports with tax returns. Any inconsistencies can trigger investigations, making meticulous record-keeping a necessity. Using automated software for reselling can help streamline this process.

To comply, you’ll need to provide Vinted with your TIN and other identification details. Failure to respond to repeated warnings may result in account removal. Additionally, Vinted must send you an annual summary of the data they’ve reported by 31 January each year. It’s essential to review this summary for accuracy and request corrections if needed, as tax authorities will use this information to assess your obligations.

Even if your sales fall below the reporting thresholds, it’s wise to maintain detailed records of all transactions, fees, and expenses. This not only supports DAC7 compliance but also simplifies VAT declarations. Tax authorities may still evaluate your activities to determine if you qualify as an entrepreneur for VAT or income tax purposes. These reporting rules highlight the importance of staying on top of your sales and VAT thresholds.

VAT Registration Thresholds Across EU Member States

VAT Registration Thresholds Across EU Member States for Vinted Resellers

Country‑Specific VAT Thresholds

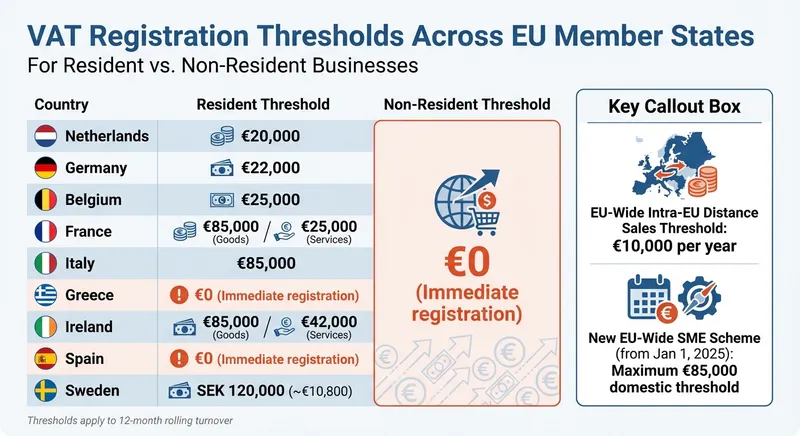

VAT registration thresholds vary across EU member states. In the Netherlands, for example, residents must register if their 12-month turnover surpasses €20.000,00 under the Small Businesses Scheme (KOR). This turnover includes all earnings - whether from platforms like Vinted, other online marketplaces, or offline sales.

In Germany, residents face a threshold of €22.000,00 if their turnover stayed within that limit last year, and current estimates remain under €50.000,00. France and Italy both set the bar at €85.000,00 for goods, while Spain and Greece require immediate registration without any threshold. Starting 1 January 2025, a new EU-wide SME scheme introduces a maximum domestic threshold of €85.000,00 for small business exemptions.

For non-resident businesses, the threshold is zero - VAT registration is mandatory from the moment the first taxable supply is made. Additionally, a separate EU-wide threshold of €10.000,00 applies to intra-EU distance sales of goods and digital services to consumers. If your sales remain below this amount, you apply your local VAT rate. Once exceeded, you must switch to the VAT rate of the buyer's country.

| Member State | Resident Threshold | Non‑Resident Threshold |

|---|---|---|

| Netherlands | €20.000,00 | Nil |

| Germany | €22.000,00 | Nil |

| Belgium | €25.000,00 | Nil |

| France | €85.000,00 (Goods) / €25.000,00 (Services) | Nil |

| Italy | €85.000,00 | Nil |

| Greece | Nil | Nil |

| Ireland | €85.000,00 (Goods) / €42.000,00 (Services) | Nil |

| Spain | Nil | Nil |

| Sweden | SEK 120.000 (approx. €10.800,00) | Nil |

How to Monitor Your VAT Thresholds

To avoid breaching VAT thresholds, keeping track of your rolling 12-month turnover is essential. This involves calculating your total revenue over any 12-month period. Once you cross the threshold, VAT must be applied starting from the specific transaction that pushed you over the limit.

For cross-border sales, categorise transactions by the buyer's country to monitor the €10.000,00 intra-EU distance selling threshold. If this limit is exceeded, you must apply the VAT rate of the buyer's country to all subsequent sales. Tools like accounting software or ERP systems can simplify this process by automatically tracking sales and adjusting for varying VAT rates across countries. If you're unsure, consulting an accountant or software provider can ensure your system is ready to manage destination-based VAT requirements.

Voluntary VAT Registration

Even if your turnover is below the threshold, you can opt for voluntary VAT registration. This allows you to reclaim input VAT on business expenses such as shipping supplies, packaging, or professional services. However, it also means you must charge VAT on all your sales and file regular VAT returns.

Voluntary registration can be beneficial if you're making significant investments in your business and want to recover the VAT on purchases. It’s also worth considering if you anticipate exceeding the threshold soon, as early registration can simplify the transition and help you establish solid record-keeping habits. Weigh the administrative effort against the potential savings to determine if it’s the right choice for your business.

Efficient sales tracking is crucial for managing VAT obligations and ensuring compliance with these guidelines. Proper tracking lays the groundwork for smooth VAT-related processes down the line.

VAT Treatment for Used Goods Resellers

What is the Margin Scheme?

The margin scheme allows you to pay VAT only on the profit you make from reselling second-hand goods, art, antiques, or collectibles. Instead of calculating VAT on the entire sales price, it's applied solely to your profit margin - the difference between what you paid for the item and what you sold it for. This scheme is applicable when goods are purchased from private individuals or sellers who didn’t charge VAT on the original transaction. To qualify, the goods must have been acquired within the European Union.

You can calculate VAT using the Individual Method, which applies VAT to each item separately, or the Global Method, which calculates VAT on your total profit. For categories like clothing or books - common on platforms like Vinted - the global method is often required.

If you sell an item at a loss, there’s no VAT to pay, but you also can’t claim a refund for the negative margin. For purchases over €500, it’s a good idea to get a signed statement from the seller confirming that VAT wasn’t deducted.

Standard VAT Rates vs. Margin Scheme

The choice between standard VAT and the margin scheme can greatly affect your pricing. With standard VAT, tax is calculated on the full sales price. Under the margin scheme, VAT is based only on your profit margin. Here's an example to illustrate the difference:

Imagine you buy a vintage jacket for €4.000,00 and sell it with a €1.000,00 profit. Using the margin scheme, you’d pay €210,00 in VAT (21% of €1.000,00), bringing the total price to €5.210,00. With standard VAT, 21% would be applied to the full sales price of €5.000,00, resulting in €1.050,00 VAT and a total price of €6.050,00.

| Feature | Margin Scheme (21% VAT) | Standard VAT Scheme (21% VAT) |

|---|---|---|

| VAT Calculation | 21% of €1.000,00 profit = €210,00 | 21% of €5.000,00 total = €1.050,00 |

| Total Retail Price | €5.210,00 | €6.050,00 |

| VAT on Invoice | Not shown separately | Must be shown separately |

| Customer Reclaim | Buyer cannot reclaim VAT | Business buyer can reclaim €1.050,00 |

Business buyers often prefer standard VAT invoices because they can reclaim the input tax. This is not possible under the margin scheme. These differences in VAT treatment can influence how you price your items and issue invoices, especially for professional sellers.

VAT Obligations for Vinted Pro Sellers

For Pro sellers navigating EU cross-border transactions, VAT compliance is critical. On Vinted, Pro sellers are required to include VAT in their listing prices. Since buyer locations aren’t known at the time of listing, you should apply the highest VAT rate applicable. Once your annual EU cross-border sales exceed €10.000,00, you’ll need to charge VAT based on the buyer’s local rate, which can be managed through the One-Stop Shop (OSS) system.

When using the margin scheme, your invoices must comply with specific rules. VAT should not be itemized separately. Instead, include the mandatory phrase "bijzondere regeling - gebruikte goederen" to indicate the special scheme for used items. Additionally, your records must clearly distinguish between transactions under the margin scheme and those under standard VAT. Each item should be traceable through purchase invoices or unique identifiers to meet audit requirements.

A case in 2024 highlighted the risks of poor compliance. The European Public Prosecutor's Office uncovered a €19.000.000,00 VAT fraud scheme involving a single actor in the refurbished goods sector across six EU countries. This underscores the importance of meticulous record-keeping and compliance for professional resellers. Proper documentation not only ensures accurate VAT declarations but also protects you in case of audits or investigations.

Cross-Border VAT Rules and One-Stop-Shop (OSS)

Intra-EU Distance Selling Thresholds

When it comes to VAT registration for cross-border sales, specific thresholds determine when you need to apply VAT based on your customer's country.

For all cross-border sales within the EU (including both goods and digital services), the annual threshold is €10,000.00. If your total sales remain below this amount, you can apply your home country's VAT rate - 21% in the Netherlands. However, once your sales exceed €10,000.00, you must switch to destination-based VAT, applying the VAT rate of your customer's country.

It’s important to note that goods sold under the margin scheme are exempt from these rules.

You’ll need to monitor your total cross-border sales across all platforms since the €10,000.00 limit applies to all sales combined. As you approach this threshold, you’ll need to decide whether to register for the One-Stop-Shop (OSS) or obtain separate VAT registrations in each country where you sell to customers.

What is the One-Stop-Shop (OSS)?

The One-Stop-Shop (OSS) simplifies the process of managing VAT for cross-border sales within the EU.

Instead of registering for VAT in every EU country where you sell, OSS allows you to register in just one Member State. For businesses in the Netherlands, this means registering through the Dutch tax authority (Belastingdienst), which serves as your "Member State of Identification."

With OSS, you file a single electronic VAT return each quarter that covers all your cross-border sales. You make one payment to the Belastingdienst, which then distributes the VAT to the relevant EU countries. This system can significantly reduce your administrative burden, saving up to 95% of the work involved in VAT compliance.

The OSS operates under the Union Scheme for businesses based in the EU. If you’re a Dutch business, you can use your existing Dutch VAT identification number for OSS reporting. The system automatically calculates and applies the correct VAT rate based on your customer’s location, ensuring compliance with VAT rules in the country of consumption.

How to Register for OSS and VIES

OSS registration becomes effective on the first day of the calendar quarter following your application. If you need to start sooner, you can notify the Belastingdienst by the 10th day of the following month.

VAT returns under OSS are filed quarterly, following this schedule:

| Quarter | Period | Filing & Payment Deadline |

|---|---|---|

| Q1 | January – March | 30 April |

| Q2 | April – June | 31 July |

| Q3 | July – September | 31 October |

| Q4 | October – December | 31 January (of the next year) |

Even if you don’t have any cross-border sales during a particular quarter, you must still file a "nil return" to stay compliant. Additionally, you’re required to keep detailed records of all OSS transactions for 10 years from the end of the year in which the transaction occurred.

For B2B transactions, different rules apply. You’ll need to verify your customers’ VAT numbers through the VAT Information Exchange System (VIES), as these sales are not reported through the OSS.

Record-Keeping and VAT Declaration Requirements

Tracking Sales and Expenses on Vinted

Keeping accurate records is essential for VAT compliance. For each transaction, note the date, item description, sale price, buyer username or order ID, and payment method. Using a dedicated bank account can make monthly reconciliations much simpler. On the expense side, track costs such as inventory, Vinted platform fees (like "Item Bumps" or "Wardrobe Spotlight"), packaging materials, and postage.

If you’re using the VAT Margin Scheme for second-hand goods, you’ll need a detailed "stock book" to document the purchase and sale prices of each item. This is crucial as VAT is calculated on the profit margin rather than the total sale price.

Additionally, business records must be kept for five years following the relevant tax return deadline. For OSS-related transactions, retain records for 10 years from the end of the transaction year.

| Record Category | Key Details |

|---|---|

| Sales Data | Date of supply, type of supply, sale price (excluding tax), VAT rate applied, VAT amount payable |

| Customer Info | Member State of consumption, customer name/address, evidence of residence |

| Expenses | Receipts for inventory, platform fees, packaging, postage |

| Payments | Bank statements showing incoming funds, details of any payments on account |

Organized records make VAT declarations significantly easier and ensure compliance with tax regulations.

How to File VAT Declarations

Once your records are in order, the next step is filing VAT declarations. Depending on the country, VAT returns may need to be submitted annually, quarterly, or monthly. For those using the OSS (One-Stop Shop), a single quarterly return will cover all cross-border sales across the EU. Key deadlines are: 30 April for Q1, 31 July for Q2, 31 October for Q3, and 31 January for Q4.

When filing, you’ll need to calculate:

- Output VAT: The VAT you’ve charged customers.

- Input VAT: The VAT you’ve paid to suppliers.

You’ll also report intra-EU supplies and acquisitions. In the Netherlands, OSS returns are submitted via "Mijn Belastingdienst Zakelijk". All OSS returns must be filed in euros, and if you’ve used another currency, apply the European Central Bank’s exchange rate for the last day of the reporting period.

If you’ve had no activity during a reporting period, a nil return must still be filed. Mistakes in previous returns can typically be corrected in subsequent returns within three years of the original due date.

When to Consult a Tax Professional

VAT compliance can get tricky, and that’s when professional help becomes invaluable. For example, the VAT Margin Scheme requires meticulous record-keeping, so consulting a tax expert is often a good idea.

If you’re managing cross-border obligations through the OSS, professional advice can be especially helpful. This is particularly true if you’re dealing with the reverse charge mechanism or need a tax representative for a non-established business. Additionally, if your cross-border sales approach or exceed the €10,000.00 threshold, an accountant can guide you on whether to register for OSS or obtain separate VAT registrations in each country where you sell.

Conclusion: Key Takeaways for VAT Compliance

Steps for VAT Compliance

Navigating VAT compliance begins with keeping a close eye on the €10.000,00 threshold for cross-border sales within the EU. Once your turnover surpasses this amount, you must apply the VAT rate of the buyer's country instead of your own. Registering for the OSS system simplifies the process by allowing you to file quarterly VAT returns in one place, reducing paperwork. For used goods, consider the Margin Scheme to tax only your profits, but ensure you maintain thorough records to validate your calculations. For B2B transactions, verify VAT numbers through the VIES system and remember to store all VAT-related records for at least 10 years. These practices integrate seamlessly into your daily VAT management on Vinted.

Using Tools Like VintiePlus

Handling VAT compliance can be especially challenging for high-volume resellers. Tools like VintiePlus can make this process much more manageable. It offers continuous marketplace monitoring and automated purchasing of underpriced items, saving you time and effort. With its advanced analytics, you can track your gross sales income precisely, ensuring your digital records meet tax authority requirements. Automated tracking also helps you monitor your turnover and take timely action as you approach the VAT registration threshold.

Final Tips for Success

Staying informed about VAT rule changes is essential. For example, starting 1 July 2026, a fixed import duty of €3,00 per product type will apply to certain e-commerce shipments. Adjust your pricing to account for differing VAT rates across EU countries. For complex situations, such as using the Margin Scheme or managing OSS filings, seek advice from a tax professional. As Jenny Longmuir, Copywriter at Taxually, advises:

"Use tax automation and stay informed to manage VAT compliance across jurisdictions and reduce risk in your e-commerce operations".