Selling across borders? Here's what you need to know: VAT and import duties can impact your profits and compliance. If you're shipping goods into or within the EU, taxes apply based on value, origin, and destination. Key changes since July 2021 include VAT on all imports, even those under €22. For shipments over €150, customs duties kick in too.

Quick Takeaways:

- VAT applies to all imports into the EU, regardless of value.

- Duties apply to shipments over €150, based on product category (e.g., clothing up to 12%, shoes up to 17%).

- Use tools like OSS/IOSS for simplified VAT reporting across EU countries.

- Shipping costs are taxable, included in the customs value for VAT and duties.

- Ensure accurate HS codes and obtain an EORI number for customs clearance.

Mistakes in tax handling can lead to delays, penalties, or rejected shipments. Automating compliance with systems like IOSS or tools such as VintiePlus can save time and reduce errors. Stay ahead by understanding thresholds, VAT schemes, and refund processes.

Why International Shipping Has Duties & VAT | Customs Explained

What Types of Taxes Apply to Cross-Border Shipments?

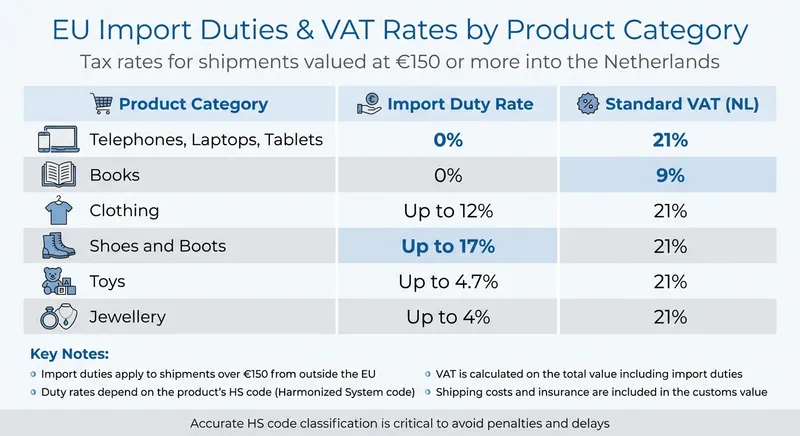

EU Import Duties and VAT Rates by Product Category for Cross-Border Resellers

When shipping goods internationally, two primary taxes come into play: VAT (Value-Added Tax) and import duties. Unlike domestic transactions, where only local VAT is involved, cross-border shipments require careful management of both taxes. These depend on the shipment's origin, destination, and total value. Import duties are calculated first, followed by VAT, which includes the value of the duties as part of the taxable amount. Below, you'll find an overview of how VAT and import duties are applied to cross-border shipments.

VAT: Definition and Application

In the EU, VAT applies to nearly all goods and services. For Dutch resellers, the standard VAT rate is 21%, while a reduced rate of 9% applies to items like books. The way VAT is applied depends on whether you're selling to businesses (B2B) or consumers (B2C).

- B2B Sales Within the EU: If your customer has a valid EU VAT number, you typically don’t charge VAT. Instead, the reverse charge mechanism applies, shifting the responsibility to the buyer.

- B2C Sales Within the EU: If your annual distance sales stay below €10,000, you can charge the VAT rate of your home country. However, once this threshold is exceeded, you must apply the VAT rate of the customer’s country.

For goods imported from outside the EU, VAT applies to all commercial shipments, regardless of their value. For example, a USB cable shipped from China costing €4.95 with €3.80 for shipping will incur €1.83 VAT (21% of €8.75). This rule has been in effect since 1 July 2021, when the EU removed the €22 exemption for small parcels.

Import Duties: Calculation Methods

In addition to VAT, import duties are another key cost in cross-border shipping. These duties apply to shipments from outside the EU valued at €150 or more. The duty rate depends on the product's HS code (Harmonized System code), with rates ranging from 0% to 17% depending on the product category.

Here's a quick look at some common product categories and their corresponding import duty rates:

| Product Category | Import Duty Rate | Standard VAT (NL) |

|---|---|---|

| Telephones, Laptops, Tablets | 0% | 21% |

| Books | 0% | 9% |

| Clothing | Up to 12% | 21% |

| Shoes and Boots | Up to 17% | 21% |

| Toys | Up to 4.7% | 21% |

| Jewellery | Up to 4% | 21% |

The customs value, which is used to calculate import duties, includes the purchase price, shipping costs, and insurance to the EU border. For example, a bag purchased from the UK for €199, with €25 shipping and €10 insurance, results in a customs value of €234. At a 3% duty rate, this equals €7.02 in import duties. VAT (21%) is then applied to the total (€241.02, which includes the duty), adding €50.61 in VAT. Combined, the customs charges amount to €57.63.

Accurate use of the correct HS code is critical. Misclassification can lead to incorrect duty calculations, potential customs delays, or even fines.

When Do Resellers Need to Register for VAT and Tax IDs?

Resellers in the Netherlands need to register for VAT (BTW) and obtain relevant tax IDs when their sales or imports hit specific thresholds. For EU distance sales under €10,000 annually, Dutch VAT can be applied through the standard tax return.

However, once the €10,000 limit is surpassed, you must start charging VAT based on the customer's country rate from the first invoice exceeding the threshold. At this point, you have two options: register for VAT in each applicable EU country or use the Union scheme through the One-Stop Shop (OSS) for a single quarterly VAT filing.

If you store goods in another EU country - like using Amazon FBA in Germany - you must register for local VAT, regardless of your turnover. Even with the Dutch small business scheme (KOR), which applies to turnovers below €20,000, EU VAT rules kick in once you exceed the €10,000 threshold. This makes streamlined schemes like OSS and IOSS essential for managing compliance efficiently.

Understanding the OSS and IOSS Schemes

The OSS and IOSS schemes are designed to simplify VAT reporting for EU distance sales and imports. With OSS, your Dutch VAT number (BTW‑nummer) can cover all EU VAT obligations through a single quarterly return. Studies suggest this approach can reduce administrative burden by up to 95%.

The IOSS scheme is particularly useful for businesses involved in dropshipping or importing goods from outside the EU. IOSS allows you to collect VAT at the point of purchase, which means goods can pass through customs without additional import VAT charges. An intermediary manages the monthly VAT returns and a single payment, further easing the process.

For non-EU businesses wanting to use IOSS through the Netherlands, appointing a Dutch-based intermediary - such as a tax adviser - is required for registration and filings. The only exception is for Norwegian companies shipping directly from Norway, as they benefit from a mutual assistance agreement that removes this requirement.

EORI and Other Required Tax IDs

In addition to VAT registration, resellers handling physical imports and exports must obtain an EORI (Economic Operators Registration and Identification) number for customs clearance. For example, when importing goods from China or the UK, both your BTW‑nummer and EORI number are necessary to ensure smooth processing.

Foreign resellers without a Dutch establishment must submit the 'Registration form Foreign companies' to the Dutch Tax Administration's International Issues department. OSS registration also assigns specific identification formats, such as IOSS numbers (e.g., IMxxxyyyyyyz) and Non-Union numbers (e.g., EUxxxyyyyyz). Each scheme allows for just one Member State of Identification, valid for the current year and the following two years.

sbb-itb-d4aa959

How Do Shipping Costs and Returns Affect Taxes?

In the Netherlands and across the EU, shipping costs are included in the taxable total. This means VAT is calculated on the combined amount of the product price, shipping fees, delivery charges, packaging, and any related travel costs. For example, if you sell a vintage jacket for €80,00 and charge €8,00 for shipping, VAT will be applied to the full €88,00. The tax rate for shipping matches the rate applied to the product itself.

How Shipping Costs Are Taxed

When it comes to EU distance sales, the VAT rate you charge depends on your annual sales volume. If your total sales remain below €10.000 annually, you charge the VAT rate of your home country. However, surpassing this threshold means applying the VAT rate of the destination country, including for shipping fees.

For shipments under €150 using the Import One-Stop Shop (IOSS) scheme, separately itemised shipping and insurance costs do not count toward the €150 limit. However, VAT is still applied to shipping as part of the total sale price.

For shipments exceeding €150, where the IOSS scheme doesn't apply, Customs calculates the import VAT based on the entire value of the shipment - this includes both the goods and the shipping costs - when the package enters the EU.

Understanding VAT refunds for returns is equally important, as the process varies depending on how VAT was collected.

Processing VAT Refunds for Returns

The method for handling VAT refunds depends on how the VAT was originally collected. Here’s how it works:

- If the customer paid VAT to a courier or postal service upon delivery: The customer must request the courier to submit an invalidation request to Customs. This must be done within 90 days of the import declaration. The courier will then handle the refund claim with the tax authorities.

- If VAT was collected in advance via the IOSS scheme: Customers must contact you (the seller) to initiate the refund process. You can then adjust the VAT in your next monthly IOSS return.

- If the customer refuses delivery altogether: You, or your customs broker, can claim the VAT refund from the destination country’s tax authorities.

For cases where VAT was overcharged, customers have two main options:

- Objection via courier to Customs: This must be submitted within six weeks.

- Refund request under Article 117 of the Union Customs Code: Customers can file this request for up to three years after the overcharge.

Here’s a quick table summarizing these refund scenarios:

| Situation | Who Handles Refund | Time Limit |

|---|---|---|

| VAT paid to courier at delivery | Customer asks courier to invalidate declaration | 90 days |

| VAT paid to seller via IOSS | Seller processes refund directly | Varies by seller |

| Customer refuses shipment | Broker claims from destination authorities | Subject to local rules |

| Overcharged VAT (objection) | Customer via courier to Customs | 6 weeks |

| Overcharged VAT (refund request) | Customer under Article 117 UCC | 3 years |

How to Stay Compliant and Reduce Risks

Navigating cross-border tax regulations is no small feat. It’s not just about knowing the rules - you need systems that can handle declarations, monitor obligations, and prevent costly mistakes. With mandatory electronic filing now the standard, resellers must adapt to avoid delays and penalties.

Using Automation to Simplify Compliance

Electronic filing is a must. For e-commerce shipments valued up to €150.00, you’re required to use the DECO declaration system to submit import declarations electronically. For goods exceeding this value, you’ll need to switch to DMS or AGS systems. Accessing these systems requires an Electronic Messaging Registration and specialised software.

Automation tools can massively cut down manual work. For instance, VintiePlus offers features like batch label printing and profit tracking. It calculates platform fees, shipping costs, tax liabilities, and even includes delivery, packaging, and travel expenses to give you a clear picture of your actual profitability.

Other tools can also simplify VAT compliance. The IOSS allows businesses to file a single monthly VAT return for all EU sales, while an Article 23 permit lets frequent importers defer VAT payments to their regular returns. Additionally, obtaining Authorised Economic Operator (AEO) status through Dutch Customs can speed up customs clearance processes.

Although automation makes compliance easier, staying vigilant against common mistakes is still essential.

Common Mistakes to Avoid

Some of the most frequent compliance errors come from misunderstandings about thresholds and declaration systems. For example, under-declaring item values to stay below the €150.00 IOSS threshold might seem tempting, but it can lead to audits and penalties.

Another pitfall is using the wrong declaration system. Submitting shipments under €150.00 through DMS, AGS, or Venue instead of DECO will result in rejections. Similarly, the IOSS scheme doesn’t apply to excise goods like tobacco or alcohol, which require entirely different procedures.

Not having an EORI number is another common oversight. This Economic Operators Registration and Identification number is required for businesses dealing with customs authorities. Without it, your shipments will be held up at the border.

When calculating customs value, many resellers forget to include shipping and insurance costs in the total. Customs value isn’t just the price of the goods - it also includes transportation and insurance costs up to the EU border. Missing this detail can lead to incorrect VAT calculations and compliance issues.

Lastly, incorrect commodity codes (HS or TARIC codes) can cause problems. These codes determine the import duties and VAT rates for your products. Using the wrong code could mean you’re paying too much - or too little - tax. The Tariff (DTV) or TARIC database can help you find the correct codes for your goods. Getting this right ensures smoother operations and keeps your cross-border shipping on track.

Conclusion

Cross-border shipping taxes are an unavoidable part of the reselling business. Mistakes in handling them can lead to fines or leave your customers dealing with unexpected clearance charges. The rules we’ve discussed here form the foundation of any effective tax strategy.

For shipments under €150, the IOSS system simplifies VAT collection. However, for shipments exceeding this amount, you’ll need to manage both import duties and VAT, as explained earlier. Staying compliant means having reliable systems in place to ensure accurate declarations and proper usage of identifiers like EORI numbers - essential steps to prevent costly missteps.

VintiePlus offers vintage resellers a way to tackle these challenges with ease. Its automation tools, such as batch label printing and detailed profit analytics, take care of the administrative heavy lifting. This allows you to focus on what matters most - sourcing unique inventory and managing cross-border sales across multiple platforms.